Understanding 401(k), IRA, and Roth IRA: A Beginner’s Guide to Retirement Accounts

Planning for retirement is one of the most important financial decisions you can make, and choosing the right savings vehicle can make all the difference. Among the most popular options in the United States are the 401(k), IRA, and Roth IRA. Each has unique benefits, tax advantages, and contribution rules. In this guide, we’ll break down these retirement accounts so you can make informed decisions about your financial future.

Why Retirement Accounts Matter

Unlike a regular savings account, retirement accounts provide tax benefits that help your money grow faster over time. Some accounts allow you to contribute pre-tax dollars, reducing your taxable income, while others provide tax-free withdrawals in retirement. Understanding how each works ensures you maximize growth and minimize taxes.

What Is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that allows employees to contribute a portion of their salary before taxes are taken out. Employers often match a percentage of your contributions, effectively giving you free money toward retirement.

Key Features:

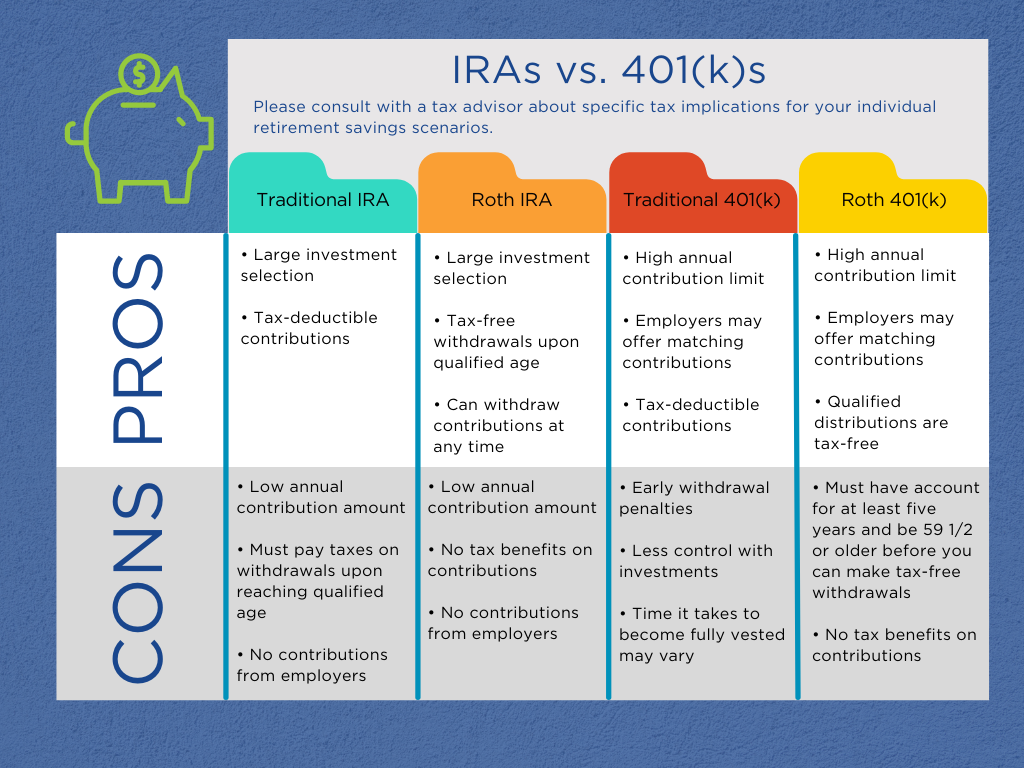

- Tax Benefits: Contributions are made with pre-tax dollars, reducing your taxable income. Taxes are paid upon withdrawal.

- Contribution Limits (2025): Up to $23,000 per year (or $30,500 if age 50 or older).

- Employer Match: Many companies match 50–100% of employee contributions up to a certain percentage of salary.

- Investment Options: Typically include mutual funds, index funds, and company stock.

Pros:

- High contribution limits.

- Employer match boosts savings.

- Automatic payroll deductions make saving easy.

Cons:

- Limited investment choices (usually set by employer).

- Early withdrawals (before age 59½) trigger penalties and taxes.

What Is an IRA?

An Individual Retirement Account (IRA) is a retirement savings plan that you open independently (not tied to an employer). It provides tax advantages similar to a 401(k) but with lower contribution limits and more investment flexibility.

Key Features:

- Tax Benefits: Traditional IRA contributions may be tax-deductible; withdrawals are taxed in retirement.

- Contribution Limits (2025): Up to $7,000 per year (or $8,000 if age 50 or older).

- Investment Options: Wide range—stocks, bonds, mutual funds, ETFs, and more.

Pros:

- Greater investment flexibility than a 401(k).

- Tax-deductible contributions (income limits may apply).

- Useful for those without access to an employer plan.

Cons:

- Lower contribution limits.

- Penalties for early withdrawals.

What Is a Roth IRA?

A Roth IRA is similar to a traditional IRA but offers different tax advantages. Instead of getting a tax deduction upfront, contributions are made with after-tax dollars, but withdrawals in retirement are completely tax-free.

Key Features:

- Tax Benefits: No tax deductions on contributions, but all qualified withdrawals are tax-free (including investment gains).

- Contribution Limits (2025): Same as Traditional IRA—$7,000 annually ($8,000 if 50+).

- Income Limits: High earners may be restricted from contributing directly.

Pros:

- Tax-free income in retirement.

- No required minimum distributions (RMDs) during your lifetime.

- Contributions (but not earnings) can be withdrawn anytime without penalty.

Cons:

- No upfront tax deduction.

- Income limits may prevent high earners from contributing directly.

Key Differences Between 401(k), IRA, and Roth IRA

| Feature | 401(k) | IRA | Roth IRA |

|---|---|---|---|

| Who Offers It | Employer | Individual | Individual |

| Tax Benefit | Pre-tax contributions | Pre-tax contributions | Tax-free withdrawals |

| Contribution Limit (2025) | $23,000 ($30,500 if 50+) | $7,000 ($8,000 if 50+) | $7,000 ($8,000 if 50+) |

| Investment Choices | Limited by employer | Wide variety | Wide variety |

| Employer Match | Yes (if offered) | No | No |

Which One Should You Choose?

For most people, the best strategy is to use a combination of these accounts:

- Start with your 401(k), especially if your employer offers matching contributions. It’s essentially free money.

- Open a Roth IRA for additional tax-free income in retirement, particularly if you expect to be in a higher tax bracket later.

- Use a Traditional IRA if you don’t qualify for a Roth or want to maximize tax deductions.

Tips for Maximizing Your Retirement Accounts

- Contribute Enough to Get the Employer Match

If your company offers a 401(k) match, contribute at least enough to receive the full benefit. - Automate Your Savings

Automatic contributions ensure consistency and help build wealth over time. - Diversify Investments

Spread your money across stocks, bonds, and funds to balance risk and return. - Increase Contributions Gradually

Whenever you receive a raise, boost your contributions by 1–2% to grow your nest egg faster. - Avoid Early Withdrawals

Withdrawing early results in penalties and taxes, reducing your retirement funds significantly.

Final Thoughts

Understanding the differences between a 401(k), IRA, and Roth IRA is crucial to building a strong retirement plan. Each account offers unique tax advantages and benefits, and using them strategically can help secure your financial future. The key is to start early, contribute consistently, and make informed investment choices. Your future self will thank you.